CLO Insider December 2022

- Capra Ibex

- Jan 1, 2022

- 4 min read

Updated: Mar 20, 2023

by Mike Kurinets, Chief Investment Officer

In December, prices in the leveraged loan market ended the month higher by 0.26 points [*1]. Overall, December didn’t hold any surprises. The leveraged loan market gains were predominately a partial reversal of the late November Omicron related selloff. This selloff took place over the final 3 days of November, as Omicron began to dominate headlines with loan prices plummeting 0.4 points.

Below is a recap of loan price performance since the end of 2020:

December’s US CLO new-issue activity [*2]

The new-issue CLO market moved at a rapid pace from August to November, as managers rushed to close deals with CLO liabilities that referenced Libor before the mandatory transition to SOFR occurring in January 2022. This rapid new-issue pace culminated with an all-time record in monthly new issuance this November.

However, December saw a clear slowdown. Since it typically takes 4 to 6 weeks between the pricing and closing of a CLO, December was likely considered too late for the CLO liabilities to close before the cut-off of January 1st. If the close of these CLOs slipped into 2022, CLO liabilities would have had to reference SOFR instead of Libor, adding basis risk [*3] to the deal.

Without a clear indication of how the market will react to SOFR-based deals, managers decided to sidestep these risks by moving up their CLO pipeline to close before the end of the year. Therefore, a week into December, new issues and resets essentially came to a complete halt.

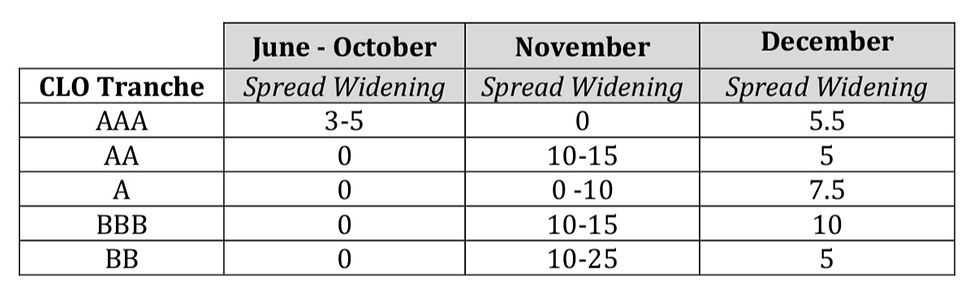

Spreads on CLO liabilities were wider in December

In our last letter we talked about how, after months of CLO spreads holding firm in the face of significant issuance volumes, November’s record setting totals finally forced spreads to widen out some. In December, with volumes significantly down, we continued to see marginal widening across the entire capital structure. The most likely explanation of the widening in December is a combination of the concerns over Omicron and the lower investor demand into year-end.

Footnotes

[*1] Based on our tracking of 907 CLOs

[*2] All data are sourced from S&P Global Market Intelligence. Both Broadly Syndicated Loan (BSL) and Middle-Market (MM) CLOs are included. On average in 2021, BSL CLOs have represented approximately 90% of total US$ CLO new issue volume.

[*3] Please see our CLO Insider Newsletter_December 2021 and CLO Insider Newsletter_November 2021 for a full explanation of the basis risk associated with transition from Libor to SOFR in 2022.

Forward Looking Statements

Some of the statements contained in this presentation constitute forward meaning of the federal securities laws. Forwardlooking statements within the looking statements relate to expectations, beliefs, projections, future plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts. In some cases, you can identify forward use of forward-- looking statements by the looking terminology such as “may,” “will,” “should,” “expects,” “intends,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” or “potential” or the negative of these words and phrases or similar words or phrases which are predictions of or indicate future events or trends and which do not relate solely to historical matters. Yo u can also identify forward discussions of strategy, plans or intentions. The forward-- looking statements by looking statements contained in this presentation reflect our current views about future events and are subject to numerous known and unknown risks , uncertainties, assumptions and changes in circumstances, many of which are beyond our control, that may cause our actual results to differ significantly from those expressed in any forwardlooking statement. Statements regarding the following subjects, among others, may be forwardlooking: the use of proceeds from our public and private offerings (as the case may be); our business and investment strategy; our projected operating results; our ability to obtain financing arrangements; financing and advance rates for our target assets; our expected leverage; general volatility of the securities markets in which we invest; our expected investments; effects of hedging instruments on our target assets; rates of leasing and occupancy rates on our target assets; t he degree to which our hedging strategies may or may not protect us from interest rate volatility; liquidity of our target assets; impact of changes in governmental regulations, tax law and rates, and similar matters; availability of investment opportunities; availability of qualified personnel; estimates relating to our ability to make distributions; our understanding of our competition; and market trends in our industry, interest rates, real estate values, the debt securities markets or the general economy. While forwardlooking statements reflect our good faith beliefs, assumptions and expectations, they are not guarantees of future performance. Furthermore, we disclaim any obligation to publicly update or revise any forwardlooking statement to reflect changes in underlying assumptions or factors, new information, data or methods, future events or other changes. This presentation contains statistics and other data that has been obtained from or compiled from information made available by third party service providers statistics or data. We have not independently verified such statistics or data.

Disclaimers:

This confidential document is for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities or partnership interests described herein. Interests in Capra Credit Management, LLC (“Capra”) partnerships may not be purchased except pursuant to the partnership’s relevant subscription agreement and partnership agreement, each of which should be reviewed in its entirety prior to investment.

Comments